If you're searching for loan relief, you're probably already exhausted, tired of EMIs that don't seem to end, tired of collection calls, and tired of feeling like there's no way out. The good news is there is a way out. And it's more accessible than most people think.

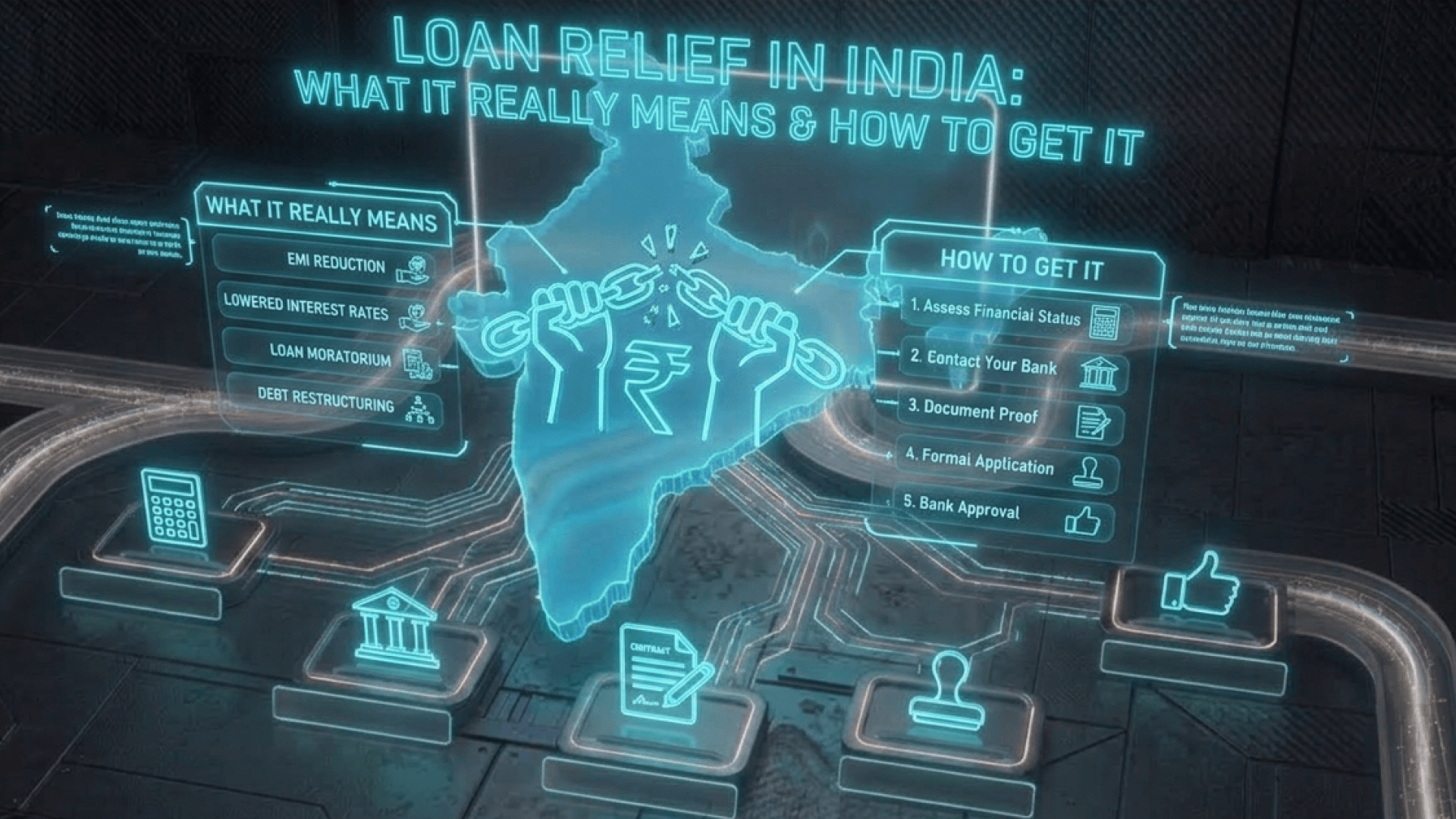

What Does Loan Relief Actually Mean?

Loan relief is a broad term that covers any process that reduces your loan burden either by lowering the outstanding amount, restructuring your repayment plan, or helping you close the loan at a reduced cost. In India, the most commonly available and effective form of loan relief for borrowers in financial difficulty is loan settlement.

People often confuse loan relief with loan waivers thinking the government will step in and wipe the slate clean. That almost never happens for regular personal loans or credit card dues. What actually works is a direct, negotiated settlement between you and your lender, where the loan is closed at an amount that's lower than what you currently owe.

This is legal. It's structured. And it works.

Why So Many Borrowers Are Looking for Loan Relief Right Now

The last few years have been genuinely difficult for a large section of Indian borrowers. Easy access to digital loans, personal loans approved in minutes, credit cards with high limits, buy-now-pay-later schemes meant that many people borrowed more than they could comfortably repay. Then came income disruptions, medical expenses, or simply the compounding weight of interest that made the loan grow faster than it could be paid down.

Today, a significant number of people are stuck paying only the interest every month, watching the principal barely move. Others have already missed several EMIs and are dealing with recovery calls that come multiple times a day. The stress of this affects everything: work, relationships, mental health, sleep.

The frustrating part is that most borrowers don't know that there's a structured solution available to them. They assume they're locked in, that the bank's terms are fixed, and that the only options are to keep paying or to default indefinitely. Neither is true.

Loan Settlement The Most Practical Form of Loan Relief

Loan settlement is when you and your lender come to a mutual agreement to close the loan at a reduced, one-time payment. Instead of continuing to pay EMIs on a loan that feels impossible to clear, you negotiate a final amount usually lower than the total outstanding and once that's paid, the loan is officially closed.

Banks and NBFCs are often more open to this than borrowers expect. The reason is simple: a prolonged Non-Performing Asset (NPA) on their books is a problem for them too. They'd rather recover a portion of the outstanding amount through a clean settlement than spend months or years chasing the full amount with no certainty of recovery.

This is why settlement works. It's not a loophole, it's a legitimate financial resolution that benefits both sides.

How the Loan Settlement Process Works

The process is more straightforward than most people expect. It starts with you sharing your loan details with the lender, the outstanding amount, and how long you've been in default or financial difficulty. A settlement platform then reviews your case and figures out what a realistic offer looks like given your specific situation and lender.

From there, they negotiate directly with your lender. This is the part most borrowers can't easily do on their own; lenders respond very differently to a professional negotiator than to an individual borrower calling in distress. Once the lender agrees to a settlement figure, you review it, approve it, make the payment, and the loan is closed.

Collection pressure naturally eases during this process, because the lender can see that a formal resolution is underway. You're not disappearing, you're settling. That changes the dynamic significantly.

Will It Affect Your CIBIL Score?

This is the question almost every borrower asks before considering settlement, and it deserves a clear, honest answer. Yes a settled loan does appear as "Settled" on your CIBIL report rather than "Closed," and this does have a temporary effect on your credit score.

But here's what most people don't account for: if you're already missing EMIs, your CIBIL score is being hit every single month right now. Every missed payment gets reported. Every month of delay compounds the damage. Continuing to default in the hope that things improve is far more harmful to your credit score over time than a one-time settlement.

Settlement draws a clear line. It closes the loan, stops the ongoing damage, and gives you a fixed starting point to rebuild from. Most people who go through settlement and then use a secured credit card responsibly, maintain a savings account, and stay disciplined with their finances see meaningful credit score improvement within 12 to 24 months.

It's a reset. Not a permanent scar.

When Is Loan Relief Through Settlement the Right Choice?

Loan settlement is not for everyone. If you're temporarily struggling but expect your income to stabilise in a few months, a restructuring or moratorium might be a better first step. But settlement is the right call when the situation is more serious when the loan genuinely feels unrepayable at the current terms, when defaults have already started, or when the interest has grown the outstanding amount to a point where regular EMIs will never be enough to close it.

If you've been making minimum payments on a credit card for over a year without the balance going down, if you've borrowed from one source to repay another, or if recovery agents are calling you daily these are signs that you need more than a budgeting fix. You need a proper resolution, and settlement is that resolution.

How Zavo Helps You Get Real Loan Relief

Zavo's loan settlement service is built for exactly this situation: borrowers who are genuinely stuck and need a clear, structured way out. Zavo negotiates directly with lenders, with no middlemen in between. This matters because it keeps the process clean, transparent, and in your interest throughout.

There are no upfront fees. You don't pay anything until the settlement actually happens. Zavo has a 97% success rate and has helped over 10 lakh verified users manage their loan situations. Once the settlement process begins, collection pressure naturally starts to ease lenders knowing a resolution is coming, and that changes how they engage with you.

Zavo also handles credit card settlement alongside personal loans, so if you're dealing with both, there's no need to manage multiple channels. And uniquely, there's a cashback offer on successful settlement, something that sets Zavo apart from most platforms in this space.

The process is fully transparent. You see the settlement offer before you commit to anything. No surprises, no pressure. You decide when you're ready.

Final Thoughts

Looking for loan relief doesn't mean you've failed. It means you're being honest about your situation and choosing to do something about it. That's actually the harder thing to do. Most people spend months or years avoiding the problem, hoping it will somehow resolve itself. It rarely does.

Loan settlement is a legitimate, legal, and often the most practical path to getting real relief from an unmanageable loan. It closes the chapter, stops the collection pressure, and gives you your financial life back.

If you're ready to explore what's possible, check your loan settlement options on Zavo. It takes a few minutes, there's no commitment, and it could be the decision that finally moves things forward.

Frequently Asked Questions

What is loan relief?

Loan relief refers to any process that reduces your loan burden — this includes restructuring, moratorium, or loan settlement where you close the loan at a reduced amount by mutual agreement with the lender.

Is loan settlement a form of loan relief?

Yes. Loan settlement is one of the most effective forms of loan relief available in India. It allows you to close your outstanding loan at a negotiated amount lower than the total dues.

Will loan settlement affect my CIBIL score?

A settled loan shows as "Settled" on your CIBIL report, which temporarily affects your score. However, if you are already missing EMIs, your score is being damaged every month. Settlement stops further damage and gives you a clear base to rebuild from.

How does Zavo help with loan relief?

Zavo negotiates directly with your lender to settle your loan at a reduced amount. There are no middlemen, no upfront fees, and the entire process is transparent from start to finish.

Can I get loan relief on credit card dues too?

Yes. Zavo handles both personal loan settlement and credit card settlement, helping you reduce what you owe and close the account legally and formally.